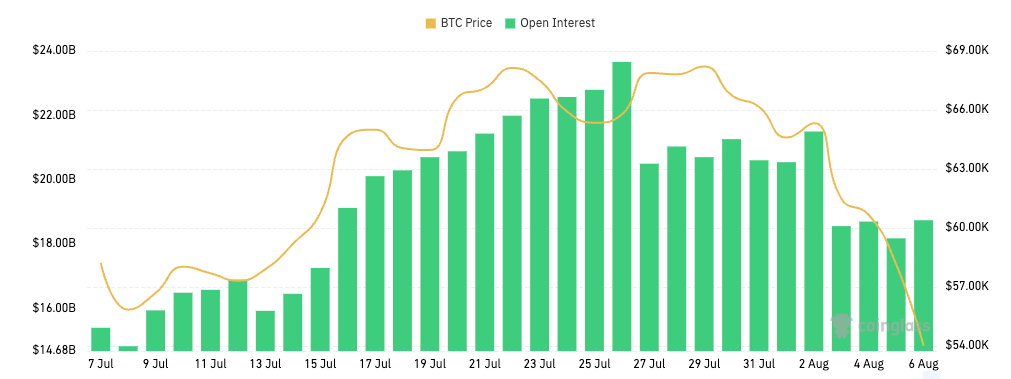

This week's crash was the biggest loss since the collapse of FTX, wiping billions of dollars from the cryptocurrency market. Bitcoin's drop below $50,000 had a dramatic impact on the futures market, with futures open interest plummeting from $31.22 billion on August 5 to $26.65 billion on August 6.

The reason for such a sharp drop in just 24 hours is likely the forced liquidation of futures positions due to margin calls. When the price of Bitcoin falls below a critical level required to maintain collateral, it typically triggers a cascade of liquidations, forcing over-leveraged traders to close their positions.

The disappearance of futures open interest seen this week indicates that a significant number of traders had bet on Bitcoin’s continued rise and were caught off guard by the sudden drop, leading to a significant reduction in their leveraged positions.

Meanwhile, the options market remained relatively stable during the price decline, with options open interest remaining roughly flat and fluctuating slightly around $18 billion over the weekend.

Unlike futures, options do not incur margin calls that immediately close out a position. Instead, traders are granted the right (but not the obligation) to buy or sell BTC at a pre-determined price. This unique characteristic allows options traders to hold positions through periods of extreme price volatility without the risk of immediate liquidation.

However, it is highly unlikely that the stability seen in options OI over the past few days is due to traders holding their positions.

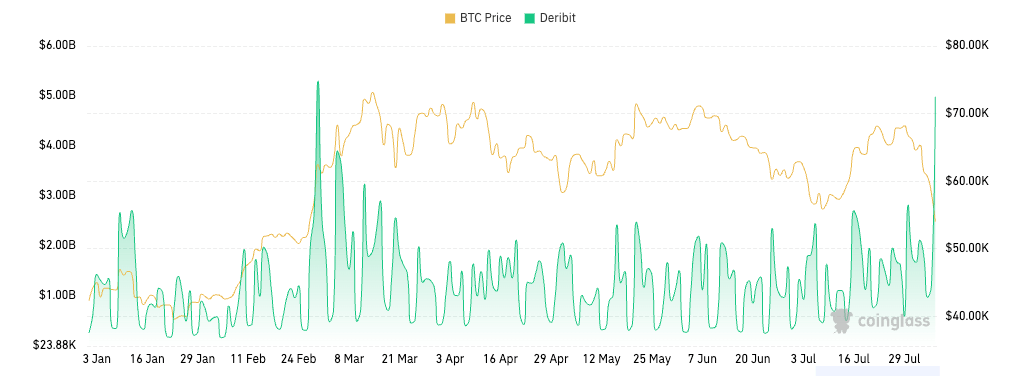

Deribit options trading volume surged from $1.22 billion on August 5 to $4.98 billion on August 6. This is the second-highest options trading volume ever recorded, after the $5.3 billion recorded in the market on February 29 this year.

A spike in trading volume indicates increased trading activity, with traders actively trading in the market. Several factors may be contributing to this phenomenon of stable open interest while trading volume is increasing.

First, during periods of high volatility, traders enter and exit positions more frequently, which means opening new contracts and closing existing ones quickly. If the number of new contracts opened and the number of contracts closed are roughly equal, OI will remain relatively unchanged even with volume spikes. High contract turnover could be due to short-term speculation, hedging, or position rolling over.

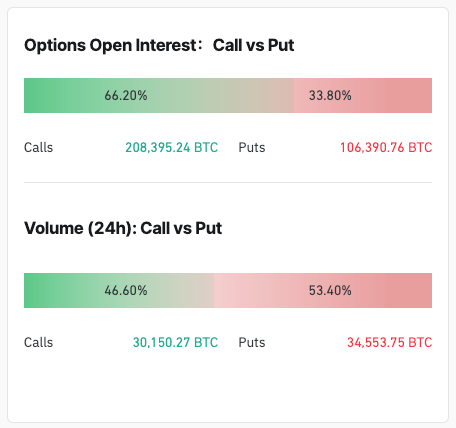

What's interesting about the options market during this period is the bias towards calls over puts, with over 66% of options open interest being calls, indicating bullish sentiment is still dominant among traders.

However, while open interest is heavily skewed towards calls, trading volume is biased towards puts. The 24-hour options trading volume from August 5 to August 6 was dominated by puts. This can be explained by traders’ immediate reaction to the price drop. When Bitcoin crashed, traders rushed to buy puts to hedge existing positions or in anticipation of further price declines in the short term.

In contrast, open interest is more reflective of traders' long-term positioning. The fact that most of the open interest is calls indicates that traders have been building these positions over time while maintaining a bullish outlook on Bitcoin's long-term prospects. These positions are not adjusted or liquidated as quickly as shorter-term trades, which is why the open interest is heavily biased towards calls.

The post Bitcoin Crash Wipes Out $5 Billion in Futures OI, But Options Remain Steady appeared first on CryptoSlate